The Great Regen CPG Divide

A tumbleweed kicks up dust as it drifts down the road. Two figures stand facing each other in a dusty boomtown. Somewhere, the intro chords to The Good, the Bad and the Ugly twang. In the battle for regenerative food systems theories of change, it’s a good ol’ fashioned western standoff.

On the left, we have emerging regenerative brands. Young, daring, and the perennial underdog, these brands are used to roughing it and are out to make a name for themselves. They are the new outlaw in town.

On the right stands Big Food. The de facto sheriff in town with a long grey horseshoe mustache - equipped with the confidence that comes from knowing that you better join ‘em, because you ain’t beating ‘em.

Regenerative agriculture, the indigenous mode of farming for millennia, spent many years in the 20th century hiding out as hippie credo. But the times, they are a-changin’. For decades, grassroots regenerative movements have been coalescing and expanding, promoting regenerative practices to farmers and marketing the value of natural, organic, and regenerative products to consumers. Supply chain shocks during COVID-19 brought greater attention to food security and access, accelerated by public interest in the health benefits of regenerative agriculture. Today, companies across the food landscape are competing for validation, customers, and shelf space in the emerging category of regenerative agriculture.

Only 1.5% of the 900 million arable acres in the US are farmed regeneratively1, so there is plenty of work to be done. In a world with a changing climate, accelerating soil degradation, significant food insecurity, and plenty of economic turmoil, there’s a big opportunity for a regenerative revolution.

But which theory of change will win the great regenerative Western standoff? What’s more important? Making the bigger, better? Or the better, bigger? Which groups gets to take the lead? The new entrants or the incumbents? Which one gets to define the direction of the movement? And, like two iconic adversaries of any western stand-off, is it really possible to have one and not the other?

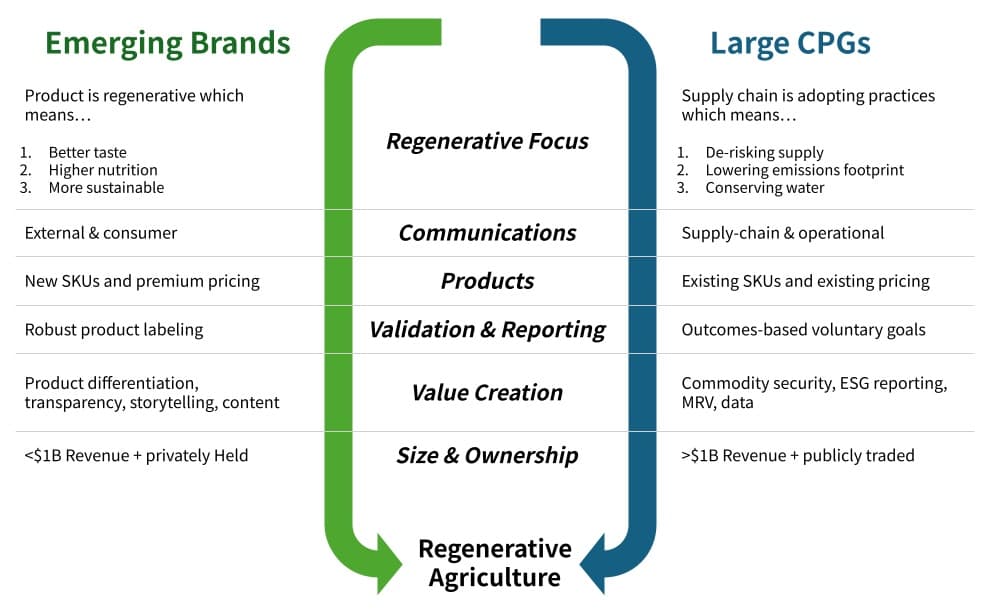

The Standoff

Emerging brands and large CPGs share shelf space and sell to the same consumers, but their pathways to regenerative agriculture couldn’t be more different.

Large CPGs are focused on shoring up supply chain resiliency while maintaining product and price consistency.

Emerging regenerative brands are working on innovative product development to bring novel and premium products to consumers.

“The Sheriffs” → Large, Multinational CPGs

On one side of this great divide are the large multinational companies that dominate the food system. Among major publicly listed food companies, 60% mention regenerative agriculture initiatives in their disclosures. The top 100 CPG companies have committed more than $3.2B toward shifting over 40 million acres of land to regenerative production. These incumbents are eyeing regenerative agriculture as a way to mitigate two existential risks: supply chain disruption and corporate reputation. For these companies, regenerative agriculture builds stronger partnerships and resilience in the face of climate change.

PepsiCo, as an example, has public standards for any “high-risk” supply, mandating environmental and human rights certifications for certain high-risk raw materials, such as palm oil and cane sugar. PepsiCo has committed over $200 million in investments to regenerative agriculture adoption in its supply chain and has a goal of sustainably sourcing key crops by 2030. These audacious, sweeping, and oftentimes vague commitments are common for companies that understand the unprecedented risks of an unstable future.

It is hard to see these huge corporate commitments reflected in product-specific changes because these massive brands are powered by equally massive supply chains. Commodity supply chain complexity renders identity preservation and farm-specific chain of custody extremely difficult, if not impossible. For many large companies, the lack of traceability limits their ability to make product-specific regenerative agriculture claims, opting instead for corporate-level reporting.

So, how do these behemoths realize the value of these regenerative investments?

Public goals, like water use, carbon emissions, or regenerative sourcing, are front and center in Big CPG corporate reporting (see Nestle, Mars, or Unilever). These companies see transitioning to regenerative systems as the new cost of doing business; if they aren’t investing in resilient systems today, they lose competitive edge and long-term security of supply.

Most big CPGs aren’t looking to change the formulation or pricing on their major, well-known SKUs. Instead, these companies are prioritizing regenerative outcomes such as environmental progress (emissions and water use), and community impact (improvements in farmer livelihood and human rights) to assess their internal risk and strengthen supply partnerships. Mars, for example, has invested in multi-year partnerships with other major agrifood companies like ADM and Riceland to scale regenerative agriculture across 150,000 acres in North America. The carbon impact of these projects is scientifically quantified using MRV technologies to contribute to Mars’ own Net Zero targets.

To meet these commitments, large CPGs are getting creative to incentivize the adoption of certain practices. These companies incentivize farmers through a variety of financing mechanisms, such as supply chain co-investments or environmental markets.

Many companies co-invest in regenerative solutions alongside farmers who are looking to make a transition to regenerative agriculture. These companies support a wide variety of commodity types, geographies, and farming operations. Nestle, as an example, has pledged over $1 billion to regenerative agriculture sourcing, with a focus on smallholder farms and rigorous outcomes measurements. Farmers who are in Nestle’s various supply sheds should benefit from additional financing provided by their massive downstream off-taker, and Nestle can claim progress towards their Net Zero sustainability goals. Other companies, like McDonald’s, support community initiatives around sustainable and regenerative knowledge sharing between farmers.

Environmental markets are a popular tool to incentivize farmers in these huge commodity supply systems because those markets help resolve the gap between information and action. Carbon, water, soil, or energy claims are measurable on farms and can be translated along the value chain. This allows large brands to provide alternative direct financing mechanisms to farmers, who otherwise might not share any direct financial or transactional relationship with the CPG companies. For example, Truterra, the sustainability business of Land-O-Lakes, has paid farmers over $9 million across almost 500,000 acres for the carbon outcomes that come from regenerative practice adoption. Truterra then sells those benefits to companies both inside and outside the agricultural supply chain to create a market for agricultural carbon outcomes.

“The Outlaws” → Emerging Regenerative Brands

On the other side of the road are emerging brands. They are laser-focused on category-specific innovation and differentiation to drive growth and consumer-first food system changes. These are smaller (but not always small), nimble, and typically privately-held CPGs that need to disrupt the status quo to achieve their goals. Most of their products carry a price premium and tout enhanced benefits over cheaper, better-known alternatives.

Emerging regenerative brands are focused on bringing novel products to market, which often necessitates scaling supply chains in new geographies, crop types, or production methods. One company, Lil Bucks, is creating a market for buckwheat, a plant traditionally grown as a cover crop. By increasing the value and demand of buckwheat, Lil Bucks is incentivizing farmers to introduce buckwheat as a value-added cover crop into their rotation, improving farmer economics, soil health, and environmental impact. Most emerging regenerative brands are focused on connecting consumers to the food they eat and supporting farmers who are already farming regeneratively. The environmental and nutrition outcomes of their unique regenerative ingredients are essential to the product differentiation and the brand itself.

Most of these brands source from direct trade of vertically-integrated supply chains that allow identity preservation and farm-level traceability, which allows emerging regenerative brands to use rigorous third-party certification to validate their regenerative sourcing claims (instead of the often limited corporate reporting of their large, multinational peers). Third-party-validated regenerative claims are often paired with the USDA Organic label, human rights certifications, or other responsible supply chain seals. A common, and increasingly popular certification is Regenerative Organic Certified®, a consumer-facing label developed to confer holistic environmental and social benefits from the adoption of regenerative and organic practices. Companies like Oatman Farms have used the ROC™ certification process to validate environmental claims, such as water conservation of over a billion gallons.

The biggest advantage for emerging brands is a direct and verifiable connection back to their farmer suppliers. Nutrition, taste, and environmental stewardship are increasingly important product differentiators, but these claims require full supply chain traceability. Brands like SIMPLI, a regenerative organic pantry staples brand, work directly with farmers and co-ops to create full supply chain traceability, unlocking global farm-to-shelf connections between consumers and the producers of their food. Other brands, like Painterland Sisters and Alexandre Farmily Farm, are the consumer-facing brands of the farm business. Vertical integration gives these businesses greater control over the entire value chain and allows them to improve the processing of their regenerative products to hopefully create a higher nutritional value than conventionally processed alternatives.

Successful regenerative brands take advantage of verified quality to build trust and loyalty with their consumers, and that trust is hard-earned. The economics of emerging CPG, especially for regenerative brands, can be incredibly challenging. Because these supply chains are often nascent and require significant levels of identity-preservation and physical segregation, many regenerative brands have significant upfront costs to build, buy, or operate the collection, processing, and distribution infrastructure necessary for their claims. The middle of the supply chain, where these brands operate, can represent up to 40% of supply chain costs, with the least amount of external investment activity.

Consumer price premiums are often the answer for most emerging regenerative CPGs to keep business economics right-side-up. These companies leverage storytelling, transparency, and validated claims to market their brand and the benefits of regenerative sourcing. PACHA, a regenerative gluten-free bread company, has robust on-package and online resources to educate consumers about the production and processing of their products. After engaging with the brand, consumers will hopefully have a clear understanding of how this specialty product was made, and most importantly, why high quality means a little higher cost.

This town ain’t big enough for the two of us. Or is it?

While these two players in the regenerative movement circle each other, what are the implications for the rest of the market?

Consumers are distrustful of Big Food. These companies have reaped the benefit of decades of degenerative, conventional agriculture, limited domestic regulation for nutrition, and rising prices due to inflation. Emerging brands, on the other hand, are trying to scale with a cost-plus business model that is only accessible to a small base of consumers willing to pay a premium for a regenerative product.

Consumers can only send demand signals for products they can choose between. When emerging brands and large CPGs compete for shelf space, the consumer has the option between price and quality. Emerging regenerative brands bring innovation and heightened consumer choice to the retail landscape, while large companies stabilize markets once consumers signal their demand for it. Large CPGs also end up acquiring many successful emerging brands to capitalize on specialty SKUs without needing to build those innovations in-house.

In these ways, large brands and small brands exist in paradoxical symbiosis. Emerging brands are tastemakers, providing new products and radical transparency to consumers, while large CPGs are market makers, creating scale and mainstream consumer awareness of new category-disrupting innovations.

Here, we come back to the sheriff and the outlaw, dependent on their shared rivalry. Maybe we need to make the bigger, better AND the better, bigger? If we can differentiate between these two sides of the same coin, we can evaluate the regenerative progress of these two styles of CPG based on integrity and authenticity. Transitioning the food system to regenerative, sustainable, and resilient farming practices is not an if but a when. There is too much excitement and too much at stake not to make it happen. What, how, and when it happens remain to be seen. Until then, I guess we can all keep watching these opponents engage in their unavoidable, perpetual, and codependent standoff.

I'm Laura Klein 👋 Co-founder and CEO at Terra Nexus Ventures. I've spent my career at the climate-food-health intersection and believe that regenerative agriculture systems are imperative to the future of food. I help companies in the food value chain improve collaboration, increase transparency, and build resiliency to support regenerative farmers and offer more nutritious products to consumers.

Editor's Note: The views expressed in this article are the author's alone and do not necessarily represent those of ReGen Brands.